This article was originally published on Cryptocurrency Hub.

Blockchain and cryptocurrencies have had a tremendous year in the media. The technology that was for a long time confined to the backwaters of tech has exploded into the public sphere in style. Dozens if not hundreds of Blockchain companies have been founded in recent months. Governments and central banks around the world are paying attention and have started countless Blockchain initiatives. But most stunningly, a seemingly endless stream of cryptocurrencies have debuted, and the values of these currencies have soared.

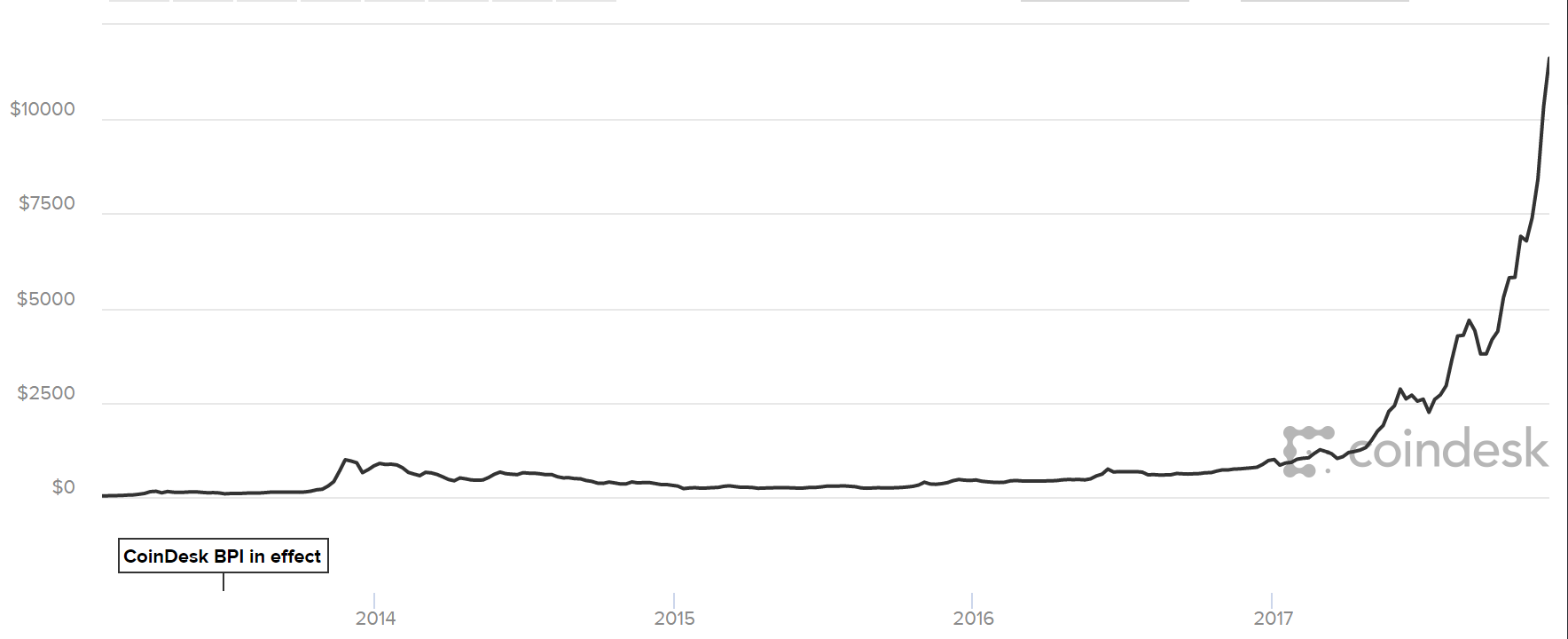

Bitcoin prices has soared from $20 in February 2013 to highs of $11,000 this month. Ethereum prices have soared from $0.95 in January of 2016 to highs of $400 recently. The list goes on.

The development of tokens — commonly referred to as cryptocurrencies — represents a tremendous innovation in the world of tech. Not only are these tokens a new way to finance a company, they are also a new way to monetize and share value. Tokens are an innovation uniquely tied to the structure of the modern web.

The soaring prices of these tokens looks by all measure to be a bubble. A financial bubble is characterized by a rapid escalation in prices of a good over and above its historical intrinsic value. We’ve had many of these historically, most famously the tulip mania in Holland in the early 17th century.

So is it boom or bust for cryptocurrencies, and are cryptocurrencies a disruptive innovation here to stay? Or, are they destined to be a interesting chapter in the books of history?

The Optimistic View

Cryptocurrencies as a paradigm shift and game-changer

The “Crypto-optimist” will believe one, some or all of the following premises:

- Decentralization is the future of societies.

- Most exchanges of value don’t need intermediaries or guarantors.

- Currencies don’t need to be government-backed to be sustainable.

- Tokens are a long overdue disruption in financing companies.

Optimists will argue the fundamentally decentralized nature of tokens enables peer-to-peer exchange of value instantly, without constraints at any time and at any place — and that this, by itself, is revolutionary. So for example if you wanted to transfer $100,000 dollars from the US to the UK, from say Bank of America to Barclays, you’d instantly hit layers of bureacracy and paperwork. But, you could send $100,000 worth of Bitcoin from one wallet to another instantly. In many contexts this is definitely tremendously valuable.

But the most compelling aspect of tokens is that while they are non-dilutive to founder equity, they still allow token investors to purchase a share in the company’s future success, making tokens a type of equity. In “initial coin offerings” a company sells a portion of its tokens to the public to raise money to finance its operations and grow its business.

In a sense tokens are equity financing in the same way that venture investment is, except that you are buying equity in the protocol and not in the company. Because the number of most tokens is capped (for various reasons) each token you have is a percentage share in the equity of the protocol. While that might be a tiny share (1000 tokens out of 1 billion), it’s a share nonetheless.

As Union Square Ventures has pointed out, the value of the protocol will always grow faster than the value of the applications built on top of it, creating “fat protocols.” Thus, for the first time retail investors can purchase “equity” at the earliest stages for emerging tech companies working in Blockchain and profit from VC-like returns. Cryptocurrencies bring the best of crowdfunding and equity financing together.

So as an optimist you can argue that this isn’t really a bubble at all. Any time you are arguing a bubble is forming you compare the current price trends with a historical baseline price for an asset (which is said to reflect the true value). What is the “correct” baseline price for cryptocurrencies? We do have some past data, but that data was before mainstream adoption for most part, so in reality we have no baseline to speak of.

Instead, the optimist will argue that we’re witnessing the creation of whole new ecosystems of value and mini-economies, and new paradigms for investing and financing. Sure prices might be a little high but they’ll cool off.

The Pessimistic View

The bubble will pop and tokens will be regulated to the history books

Many people I think secretly hold this view, and some not so secretly such as Jamie Dimon, the CEO of JP Morgan. Pessimists take issue with premises 1–3 above. Especially premise 3. Jamie Dimon specifically said that he “doesn’t believe in non-fiat currencies.” A fiat currency is a government-backed currency and legal tender, but not a currency pegged to the value of any physical commodity. This contrasts to the Gold Standard where historically currencies were pegged to the value of gold.

The absence of a central authority and “government-like” entity does make many people nervous. Many protocols have forked multiple times recently and no mechanism really exists for governing this process or reversing it. Similarly, fiat currencies have central banks that use monetary policy tools to keep prices within a certain range (for floating currencies). In contrast, many people criticize the volatility of cryptocurrencies.

Aside from these issues there is an additional criticism that you can leverage against many tokens. Money is traditionally described to have three functions: a medium of exchange, unit of account and store of value. The vast majority of cryptocurrencies are currently only stores of value. Their dramatic rises in price have been driven by speculation, not by underlying shifts in behaviour.

Most cryptocurrencies are not yet mediums of exchange. That is you don’t buy other goods or services with most cryptocurrencies yet, especially Bitcoin and Litecoin (Ethereum is the exception because you typically use Ethereum to buy other tokens during an ICO). Thus, these currencies aren’t tied to underlying economic exchanges as of yet. Many of the new tokens have been designed with that purpose in mind — such as SmartContract.com’s Link Token — but as of yet many of these economic exchanges have yet to transition to or adopt blockchain technology.

The pessimist would argue that no such future state will exist. We may use distributed ledger technology and smart contracting elements of Blockchain, but we won’t need cryptocurrencies to do so they would argue. Normal currency “works fine.”

For the pessimist the paradigm of a currency is a fiat currency. Government backing and a central bank are necessary for any stable currency. That being said even most pessimists recognize that distributed ledger technology and smart contracting are useful implementations of the Blockchain.

The Realistic View

Prices will adjust but crypto is here to stay

William Janeway, an American economist and venture capitalist, in his 2012 book argued:

“Financial bubbles have been the vehicle for mobilizing capital at the scale required in the face,” he writes, of such “fundamental, intractable uncertainty.”

I think this is the correct view to hold on the current market for cryptoassets. The three main applications of Blockchain — smart contracts, cryptocurrencies and distributed ledgers — solve some thorny problems and have interesting use cases. But it is still very early days to say how things will pan out and how we will integrate Blockchain into business and government processes across the world.

Janeway argues that speculative bubbles are necessary to fuel productive innovation. In an environment where investors assess the risk-adjusted returns for a particular space over a period of time to be better than they actually are — or to put it another way they judge risk overall to be lower than it actually is — then you are likely to see significant capital flow into this space/technology.

We’ve had many examples of this. The Dotcom bubble of the early 2000s and the housing bubble of 2007. When things go bust their is usually a period of tremendous carnage. But these speculative bubbles push investors to invest in more novel companies and technologies, and the companies founded in bubbles that IPO are valued higher than those founded outside of bubbles.

While most companies built in bubbles go bust, the survivors are often game-changers. Alphabet (Google) is a good example of this (founded in 1998 in the run up to the Dotcom bubble).

A realistic view of the current state of cryptocurrencies involves being comfortable with the idea that this is a speculative bubble. A realist sees a future state where we do integrate cryptocurrencies into many of our business and governement processes. The question is when this transition will happen, but if you’re a realist you hold that it will happen. It is this transition that supports the long-term value of tokens over time, as well as the value of the network around a protocol.

Conclusion

Perhaps defining yourself as an optimist, realist or pessimist is not useful for your own thinking. But given the uncertainty involved in crypto, if you are investing heavily in tokens or plan to, it makes sense to think about your portfolio allocation. Because if it all goes up in smoke and you’re not diversified, life will be interesting to say the least.

Leave a Reply