This piece was originally published in my newsletter Emergent.

Latin America’s market of 650 million people has long tempted entrepreneurs and investors as a region on the cusp of huge economic growth and an exciting place to innovate and invest. Despite this, the region has struggled through numerous crises ranging from civil wars, poor governance and inflation. In fact, GDP per capita has fallen from a peak of $10,400 in 2014 down to $7,400 in 2020 – a steep 30% decline. However, one major bright spot in LATAM’s economic story is the rapid digital transformation underway. LATAM is following in Southeast Asia’s footsteps in this regard with rising mobile phone penetration and a young tech-native population that has unleashed a wave of entrepreneurial energy across the region. One of the flagship companies leading this new entrepreneurial surge in LATAM is Colombian delivery startup Rappi.

Rappi is a Latin American Super App offering users rapid delivery of a range of items (food, medicine, clothes), a suite of financial services and a platform for booking experiences from travel to concerts and hotel stays. Rappi was founded in 2015 and since then has scaled rapidly:

- Has 10 million monthly active users

- Live in 250 cities across 9 countries in the region – Colombia, México, Costa Rica, Perú, Ecuador, Chile, Argentina, Uruguay y Brasil

- Raised over $2 billion in financing to date

- 200,000 delivery drivers

- 100,000 merchants

In a short span of time Rappi has emulated notable startups worldwide such as Meituan, Grab, Getir and combined aspects of their business models and products to create Latin America’s first Super App.

Products

Rappi initially launched as a food and grocery delivery platform but has quickly evolved into a Super App offering a broad range of complementary services to its users. Like all Super Apps, Rappi has grown its product offering as its user base has scaled.

Rappi offers all kinds of products including:

- Rappi Food

- Rappi Mall

- Rappi Medicine

- Rappi Cash

- RappiBank

- RappiTravel

Rappi’s product evolution has followed the playbook laid out by Grab and GoJek (now GoTo) in Southeast Asia closely. Initially the company focused on grocery and food delivery and building out a strong logistical network of drivers as well as building its initial userbase. After building out this core infrastructure and its initial userbase Rappi began layering on services that could sit on top of its network of drivers at no additional cost to the business such as medicine delivery, food delivery, alcohol delivery, grocery delivery and more. Finally – much like Grab and GoJek – as Rappi has captured more and more of a consumer’s discretionary spending through its application, the logical next phase of its expansion has been into financial services.

Rappi is early in its expansion into financial services and doesn’t have a full digital banking license like Grab or GoTo do. In fact, Rappi’s financial services remain fairly limited today. With Rappi cash users can pay Rappi with their credit or debit cards and have a delivery driver come to their home with the equivalent amount in cash – cash delivery. With RappiPay users can conduct peer-to-peer transactions at no cost. Most recently Rappi has began offering credit cards. The company has launched Rappi credit cards in partnership with Visa in four countries over the past year – Brazil, Mexico, Colombia and Peru.

These services are limited compared to what most neobanks – such as NuBank – or even what Grab and Gojek offer to their customers today. However, Rappi’s continuing expansion in financial services is likely to see it pursue a digital banking license in the near future.

Market & Competition

Rappi has managed to grow rapidly during the COVID-19 pandemic despite the challenges it has presented. However, the LATAM region has suffered significant economic losses from the pandemic that will take years to recover and present a near and mid-term challenge to Rappi’s continued growth. In 2020, over 45 million people in the region fell back into poverty and over 230 million people fell back into the group living on less than $10 per day.

However in the long-term the pandemic will help accelerate Rappi’s business. In 2020, over 50 million people are estimated to have bought products online for the first time in LATAM – adding 50 million new potential customers to Rappi’s addressable market. By 2022 over 300 million people in the region will be ecommerce consumers – a huge market for Rappi to tap into.

The huge and growing ecommerce market in LATAM has attracted numerous competitors including:

- Glovo: The Spanish delivery startup – founded the same year as Rappi – has raised over $500 million in funding

- UberEats: Uber’s food delivery division has been a player in the region for years

- Domicilios.com: Acquired in 2014 by global food delivery giant DeliveryHero which is investing significant capital in growing Domicilios market share in the region

- iFood: The market leader in Brazil’s food delivery space

The food delivery business has strong network effects and economies of scale. As a result, the structure and margin profile of the food delivery industry naturally leads the industry towards having one or two dominant players with majority market share, such as Meituan’s 60%+ market share in China’s food delivery market. As such, the sign of a maturing food delivery market is typically consolidation and this has started to occur in the region.

Glovo exited Chile and Brazil in 2019 and UberEats exited Argentina and Colombia in 2020. In most of the smaller countries in Latin America Rappi is the market leader in food delivery such as Colombia, Peru and Costa Rica. However, the big prize in Latin America is Brazil – a country of 210 million people. In Brazil, Rappi is fighting for second place in the market and far from dominating the market.

Competition has intensified for Rappi in the bid to become the dominant food delivery platform in the region with the merger of iFood and Domicilios.com. iFood operates in over 1,000 cities in Brazil and works with 150,000 restaurants. The two companies combined claim to have the largest presence in Colombia of over 12,000 restaurants in 30 cities. The stage is set for a battle for supremacy between iFood, Domicilios and Rappi for supremacy in the food and wider delivery segment in LATAM.

Growth Opportunities

Rappi has followed the Super App playbook over the past six years pioneered by the likes of Meituan and Grab in Asia. The company can continue to grow in two main ways in the years to come:

- Geographic expansion

- Offering full-service digital banking products and services

LATAM is composed of 33 countries of various sizes. Aside from Brazil, Spanish is the dominant language across much of the region and English and French the dominant language in much of the Caribbean. This helps simplify some of the operational challenges of geographic expansion. Today Rappi is present in the 9 biggest countries in the region but the company has the scale to expand into the remaining countries in the region and dominate them. Over time, Rappi is likely to do this to grow its business.

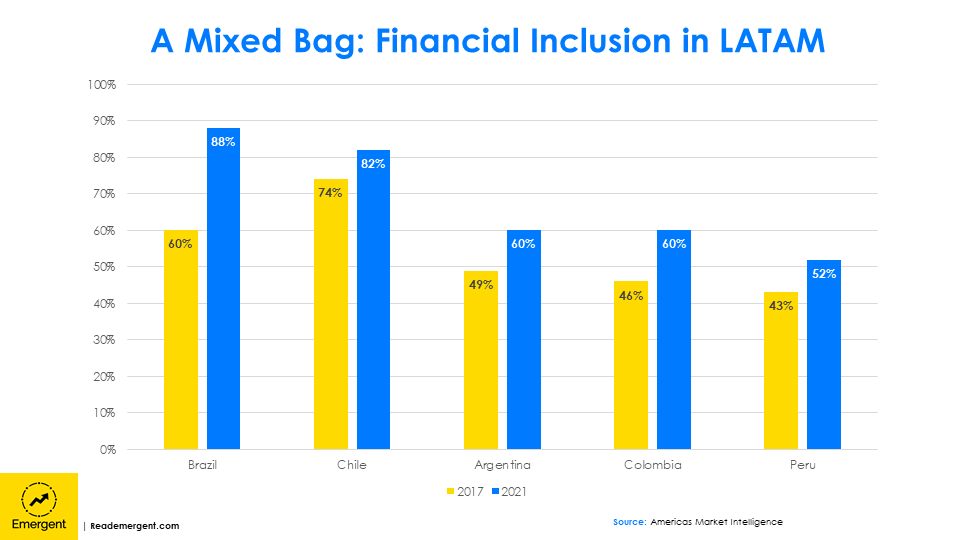

Financial services presents the most lucrative potential expansion opportunity for Rappi in the years to come. Digital banking has performed incredibly well in LATAM – particularly Brazil – and over 120 million (about 20%) of the region’s population are customers of various digital banks such as NuBank, MercadoPago, PicPay and others. Large segments of the region’s population remain unbanked today, a huge opportunity to offer banking services, credit, insurance and other products.

For Rappi to evolve into a full-service digital bank it will have to secure digital banking licenses like both Grab and GoJek have done in Southeast Asia. This will enable it to offer a full range of financial services to its consumers. Rappi is clearly on the path to turning its RappiBank division into a full-service digital bank. For example, in May of this year Rappi launched a digital insurance offering in partnership with Chubb in Mexico offering mobile, home and identity insurance.

Rappi is one of the fastest-businesses to become a true Super App, doing so in as little as six years. However, Rappi’s journey is far from over and the path ahead for it looks bright. The company is a bellwether for LATAM’s technology ecosystem and its continued success will be critical to the ecosystem’s development in the years to come.

This piece was originally published in my newsletter Emergent.

Leave a Reply