This article was originally published in my newsletter Emergent.

Globally remittances has been one of the largest and fastest growing segments of financial services for years. By 2022 remittance volume to low and middle-income countries reached a whopping $630 billion. Despite the size of this global market the remittance industry is plagued by friction and significant costs for end users. In particular, sending money to and from Africa has traditionally been a costly endeavor. However, with the African continent becoming a hotbed for fintech activity the continent has seen an explosion of new fintech startups founded over the last few years, many targeting remittances.

One of the most exciting and fastest-growing fintech startups in Africa today is Chipper Cash. Launched in 2018 by Ugandan native Ham Serunjogi and Ghanaian native Maijid Moujaled, Chipper Cash is a fintech company offering zero-fee, peer-to-peer cross-border payment services in Africa, Europe and USA through its app. The idea for Chipper was born when the founders personally faced the struggles of sending money to Africa firsthand as international students.

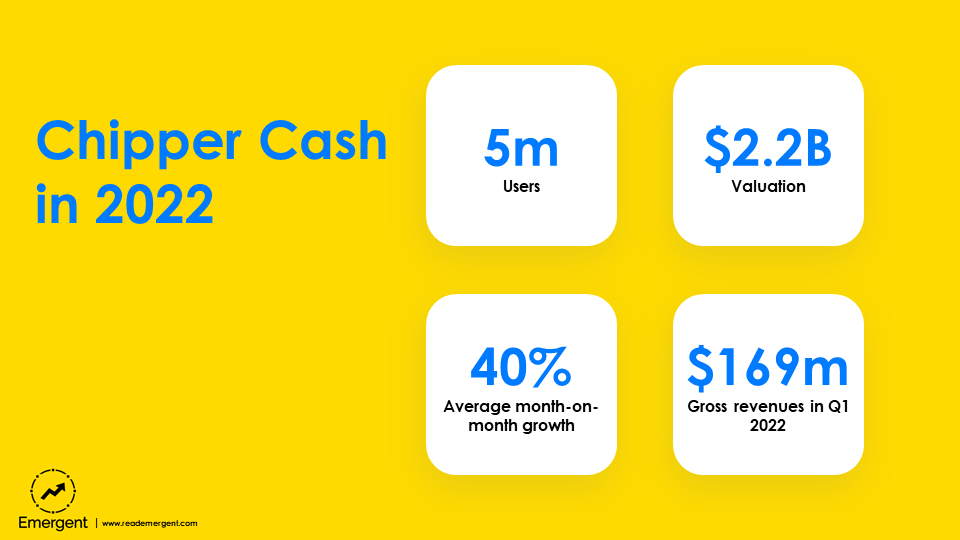

After just four years of operations Chipper Cash has become one of the fastest-growing startups in Africa. Its founders have collectively raised $337 Million across 6 rounds of funding from notable investors like the now-defunct crypto exchange FTX, Ribbit Capital, Bezos Expeditions, SVB Capital and many others. Since its founding in 2018, Chipper Cash has managed to:

- Average 40% Month-on-Month growth

- Acquire 5+ Million users to date

- Process $1.65 in total payment volume in Q1 2022

- Earn gross revenues of $169 Million in Q1 of 2022

- Achieved a peak valuation of $2.2 Billion

By the end of 2022 unfortunately Chipper Cash suffered a setback when its lead investor FTX marked down its valuation by 37.5% to $1.25 Billion and declared bankruptcy in December. Understandably, Chipper Cash had to cut back on staff (12.5% of its workforce) to preserve runway as the company gears up for further growth in 2023.

Product

Chipper Cash is a lot more than a remittance company and today offers a broad suite of services across payments, investing and business tools with remittances being the core of its offering. All of these services can be accessed via the firm’s mobile apps, which are available for Android and iOS devices. Chipper Cash’s product suite includes:

Payments

- Sending and receiving cash: Users can easily and quickly move their money across Africa or the USA/UK, in a free and fully secure manner with the lowest cross-border rates. The app offers 2% cashback on Airtime, and users can instantly top-up from anywhere and send airtime to anyone across Africa. This service also allows instant bill payments through the app, with no additional fee.

- Chipper Card: This card allows online shopping, streaming and subscriptions from anywhere around the world. This card can be used for online purchases anywhere where visa cards are accepted.

Investing

- Investing in Crypto: Bitcoin can be bought and sold across Africa, with all crypto-money and personal information securely protected. Chipper cash allows a user to instantly convert local currency to Bitcoin and connect any mobile money or bank account. The app offers 24/7 real time pricing and instant trade execution.

- Investing in Stocks: Users can build a stock portfolio by investing in fractional shares of publicly traded companies of their choice, with as little as $1. Users have access to 6,000+ US Public companies to invest in.

Business Tools

- Network API: This is a payment method that gives businesses access to 5+ Million KYC verified customers. Chipper Cash enables them to accept cross-border payments at the lowest transaction fees, and send payouts across all its markets. It has an easy and accessible dashboard that provides access to all transaction data, allows sales insights and downloading of reports. Chipper Cash’s encrypted business wallet keeps the money safe with a guarantee.

- Chipper Checkout: This allows merchants to sell on social media and messaging apps with payment links, at low transaction fees. These checkout buttons can be integrated directly with a merchant website or app. Even non-chipper users can get a fast guest checkout flow.

Business Model

As sending money to and from Africa is expensive, Chipper Cash’s business strategy involves using its free money remittance service as a customer acquisition channel. The company then upsells the same customers into other products. Chipper Cash earns its revenue from foreign-exchange fees and crypto brokerage commissions. These include fees on stock and cryptocurrency transactions, interchange fees, and payment fees.

Interchange Fees

Chipper Cash offers a virtual debit card in conjunction with Visa, which can be used to pay for goods and services at any merchant that accepts Visa payments. Everytime the card is used, an interchange fee is applied which is paid by the merchant. A typical debit card issued by Mastercard or Visa incurs an interchange fee of 0.5%, plus a fixed fee of $0.10 per transaction. This revenue is split between Chipper Cash, Visa and the local partners.

Investment Fees

Chipper Cash’s investment products allow members to purchase and sell stocks or cryptocurrencies. Users of the service may indulge in bitcoin transactions or purchase/sell shares of companies like Amazon, Netflix, etc. For each transaction through the platform, whether purchase or sale, Chipper Cash charges a 1% transaction fee.

Payment Fees

Chipper Cash charges a payment fee from businesses utilizing its Network API. The Chipper Network API allows businesses to collect payments from their customers, pay suppliers or issue instant refunds. For all payments collected by a member business, Chipper cash charges a low 1% fee.

Market

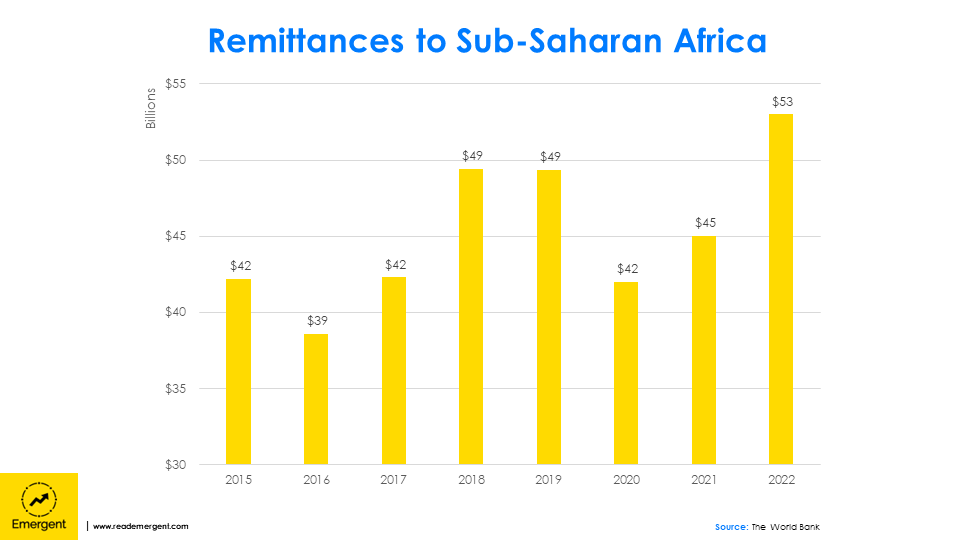

Ever since the advent of global remittances banks and payment processors have charged exorbitant fees sometimes reaching into double-digit percentages. Prior to Chipper Cash’s launch, in 2017, African immigrants reportedly sent around $41 Billion to Sub-Saharan Africa in remittances to their friends and families. Another study from 2019 revealed that 8% of people in East Africa actively send or receive payments across borders. However, only half of these payments are being made through bilateral agreements between mobile money operators.

By 2022 the remittance market in Sub-Saharan Africa grew to $53 billion and is projected to grow at 3.9% in 2023. Of this the U.S. is responsible for almost 30% of the international remittances to sub-Saharan Africa. What makes Chipper Cash’s services even more relevant in the region is the significant interest in crypto ownership on the continent. In 2021, crypto adoption in Africa rose by more than 1,000%, with peer-to-peer transaction volume standing at $105 Billion. A lot of the crypto activity on the African continent is driven by users in Nigeria, South Africa and Kenya – countries where Chipper Cash is active.

Competition

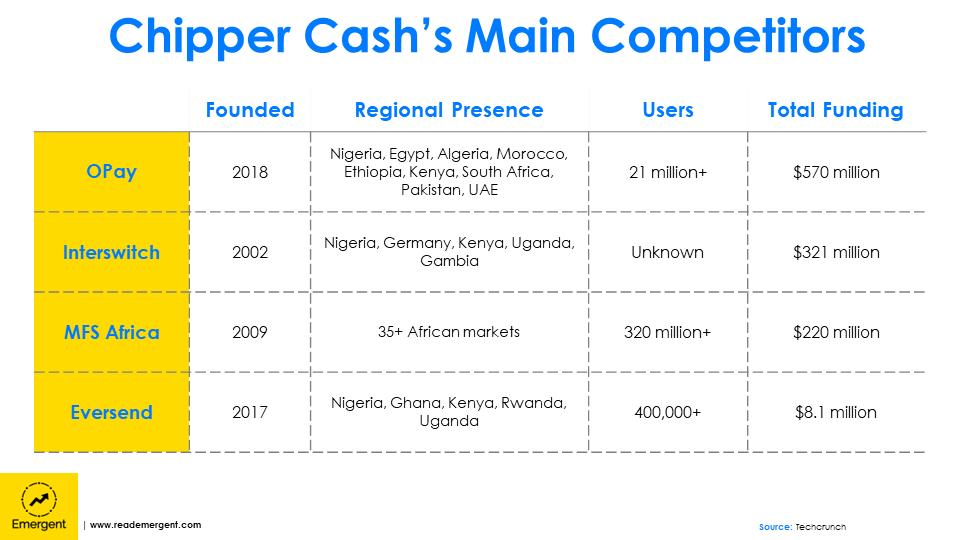

Remittances has attracted the attention of numerous companies over the years and Chipper Cash is competing against the likes of MFS Africa, OPay, Interswitch and many more companies.

OPay was founded in 2018. It is a one-stop mobile-based platform for payments, transfers, loans, savings and other essential services. Currently, it has over 18 million registered app users and 500,000 agents in Nigeria who rely on OPay’s services to send and receive money, pay bills and more. It has raised $570 Million in funding.

Interswitch has been around since 2022. It is an Africa-focused integrated digital payments and commerce company that facilitates the electronic circulation of money as well as the exchange of value between individuals and organizations. It has raised $320.5M in funding, and by May 2022, it had issued 35M+ active debit cards since its inception. It oversees transactions for 190K+ businesses each day.

With stiff competition from these players, how does Chipper Cash differentiate its services? The answer lies in its remittance offering, where it has managed to grow its user base at a rapid pace by enabling them to get rid of those fees. This strategy is complemented by Chipper Cash’s simultaneous and quick expansion into as many countries as possible to enable cross-border payments. Furthermore, the company’s products are designed to include low-income, remote populations. Chipper Cash solves issues related to inclusivity in finance by making its products affordable, accessible and easy to use.

Since Chipper’s transfer product is free for end-users, it is inherently affordable for those who can access it. Being free is a key differentiator for Chipper in an otherwise crowded payments space. In terms of accessibility, to make use of Chipper Cash’s offering, a user needs mobile money accounts and smartphones. Fortunately ,smartphones are owned by hundreds of millions of people in Sub-Saharan Africa, and the penetration rates are predicted to grow to 66% by 2025. Moreover, Chipper’s interoperability feature makes its apps widely accessible for users with accounts or wallets across a number of MNOs (like M-Pesa and Airtel) that facilitate easy account opening. Finally, Nigerians with credit cards and bank accounts can also access Chipper’s products, reducing the barriers of smartphone ownership. Chipper’s products also have a high level of usability. Its user interface is simple, easy to navigate, and intuitive for even the most basic users.

Growth Opportunities

Chipper’s growth has not come easy and the company has gone through many periods of fits and starts. After releasing its first version in July 2018 which allowed customers to send money from Uganda to Ghana at no cost, the founders struggled to raise funding in the initial stages. At the time, venture capitalists assumed that the African market wasn’t offering any attractive growth prospects.

Despite its early challenges Chipper Cash today is one of the fastest-growing fintech startups in Africa. Going forward, Chipper has several possible avenues to continue its growth including:

- Doubling down on global partnerships

- Continued geographic expansion

- Expand its fintech product suite

Chipper Cash has experimented with a few different types of partnerships so far in its journey. The company currently has a global partnership with Nigerian superstar Burna Boy, and has integrated with Twitter to support its “Tips Jar” feature for African users. Both of these partnerships are designed to help the company acquire users cost effectively and continue to power its growth. There are many further potential partnerships the company can explore to unlock its next phase of growth. Its user base of 5 million users is an attractive proposition to global businesses looking for targeted exposure to the African market and the company’s fintech products also serve as powerful financial infrastructure for global companies to take advantage of.

Besides global partnerships further geographic expansion is a logical growth path for Chipper Cash and the company has already begun the process. Chipper Cash is present in some of Africa’s biggest markets today but the continent has 54 countries. While remittances from the West are a major source of total remittance volume, a lot of Africa’s remittance volume comes from other African countries. For example, South Africa is a popular destination for migrant workers across the continent and a major source of remittances.

By expanding across the continent Chipper Cash can access a larger share of the total remittance flows. In November 2022, Chipper cash announced its intentions to buy Zambian Fintech company Zoona in order to expand cross-border payments in Africa. The deal is expected to bring to Chipper Cash new online services, a new agent network and entry to Zambia. Chipper Cash executives have also shared publicly that the deal would bring together complementary products and services, and enable the two companies to connect consumers and businesses across Africa. Finally, the company already has plans underway to expand the Chipper Visa Card across the African continent given how large the continent’s unbanked population is.

Lastly, besides geographic expansion further broadening its suite of fintech products is the final growth path for the company. To date Chipper Cash has been heavily focused on consumer fintech and remittances but the opportunity in B2B fintech is significantly larger than in consumer fintech in the long-term. Chipper Cash has already begun experimenting with business products through its launch of Chipper Checkout product. As payments increasingly go digital across the continent many businesses are struggling to play catch up and adapt to the wide range of mobile money wallets, cards and payment methods consumers want to use. Many of the continent’s largest fintech platforms have over time built products to service both consumers and businesses to build a synergistic loop improving its products on either side. The opportunity in B2B fintech is massive and competition in this segment is picking up rapidly.

Overall, Chipper Cash is a powerful example of opportunity in delivering next-generation digital financial services in emerging markets. The company has experienced breakneck growth yet barely penetrated its core market of remittances. Much of the market is dominated by legacy players like Western Union which will take time to fully displace. The company’s growth path in years to come will be an interesting one to track as it navigates the geographical complexity of the African content and the complexity of payments and financial services.

This article was originally published in my newsletter Emergent.

Leave a Reply